CSRD Double Materiality

The Corporate Sustainability Reporting Directive (CSRD) encompasses a wide range of disclosure requirements. As first reports will be due in 2025 for financial year 2024, let us have a look at a key concept underpinning the legislation! 🚦

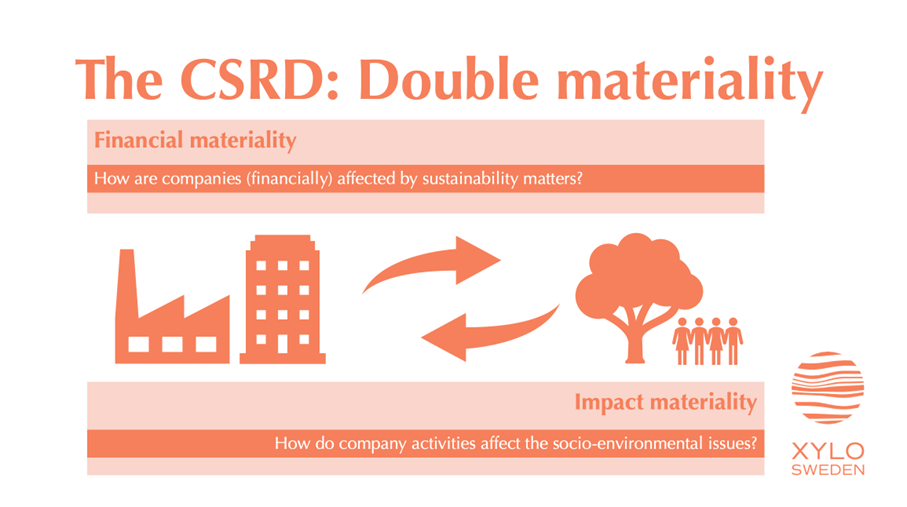

Double Materiality is a concept central to the CSRD and the introduced binding reporting standards, the European Sustainability Reporting Standards (ESRS). It refers to the notion that the company activities affect the social and environmental matters, but these sustainability matters in turn also affect the company. Thus, the double materiality is split into impact materiality and financial materiality.

Impact Materiality concerns activities which generate short or long-term, positive or negative, and active or potential impacts on the environment 🌱 and people. This is clearly connected to the Environment, Social and Governance (ESG) framework of classifying sustainability issues, as seen also in the CSRD with the proposed topical standards (the defined areas of sustainability). For example, calculating the environmental footprint of your organisation with respect to greenhouse gas emissions would fall under impact materiality.

Financial Materiality focuses on the risks and opportunities created by sustainability issues. For example, if climate change is expected to result in diminishing stocks crucial to your supply chain, or if violations of fair labour laws occur, this will have financial repercussions for your company. 🚨

One of the largest challenges is for companies to determine how all these different parameters interact and which of them are the most important. Not all areas of sustainability are relevant for all companies, thus double materiality assessment is done to identify which areas should be reported on.

If a topical standard is found to be non-material to the organization, the organization does not have to report on it (providing justification!), which creates a certain degree of reporting flexibility, especially for small-to-medium enterprises (SMEs). The purpose with this is to ensure that reporting is done on the right topic areas, but also to hold companies accountable for the impacts associated with their activities. 📣

If all these topics are making your head spin, you can book a free consultation with us, and we will help you figure things out step by step!